Making Tax Digital: what landlords and self-employed individuals need to know

From 6 April 2026, HMRC will be making the largest change to tax reporting since the introduction of Self-Assessment 30 years ago.

Taxpayers who are required to comply with Making Tax Digital (MTD) will need to keep digital records and submit their income and expenditure on a quarterly basis for their rental property and self-employment businesses. This submission will be made via a digital link using MTD approved software.

Who will be affected?

HMRC announced that the individuals affected by MTD will depend on their combined gross income levels for their rental property and self-employment businesses. You will be required to submit MTD returns:

-

From 6 April 2026, if your combined gross income is £50,000 or more

-

From 6 April 2027, if your combined gross income is £30,000 or more

- From 6 April 2028, if your combined gross income is £20,000 or more

The requirement to comply from 6 April 2026 has been based on the income reported on the 2024/25 tax returns and this will likely be the case for future tax years.

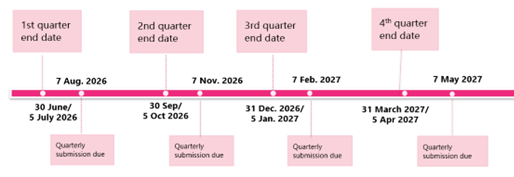

If you are required to register for MTD from 6 April 2026, the first quarter of 1/5 April – 30 June/5 July 2026 will need to be submitted by 7 August 2026 as shown in the diagram below:

Will I be exempt from MTD?

There are several scenarios where taxpayers will either be permanently excluded from MTD or whether this requirement has been deferred indefinitely or until April 2027.

| Permanently excluded | Deferred indefinitely | Deferred until April 2027 |

|

• Taxpayers who claim Married Couples Allowance or Blind Persons Allowance

• Taxpayers with a Power of Attorney or Deputyship |

• Partnerships

• Trusts, Estates, Trustees of registered pension schemes and non-resident companies • Taxpayers who do not have a UK National Insurance Number • Lloyds underwriters • Ministers of religion, distributions to shareholders in real estate investment trusts, or distributions to participants in open-ended investment companies |

• Those completing residence/remittance pages of the tax return

• Those receiving Trust or Estate income • Those claiming averaging reliefs (for example farmers) • Taxpayers claiming qualifying care relief (for example foster carers) • Non-resident foreign entertainers or sportspeople |

What do I have to do?

If you meet the reporting threshold and are not exempt from MTD, you will need to:

-

Use MTD compatible software

-

Keep digital records

-

Submit quarterly updates

-

Submit end of year adjustments for MTD income

- Submit a tax return, again using MTD compatible software

The deadline for submitting your Self-Assessment tax return is still 31st January and the tax payment due dates remain the same.

The quarterly submissions will be cumulative, so if you realise you made a mistake on your last submission, rather than amending that submission, an adjustment will need to be made on the following quarter’s submission.

The quarterly submissions will be cumulative. This means that if you realise that a mistake was made on your last submission, rather than making an amendment, an adjustment will need to be made on the following quarter’s submission. Any accounting or tax adjustments will need to be taken into account when completing your Self-Assessment tax return.

Each self-employment will be treated as a separate business for MTD, but rental properties will be grouped into UK rental property and foreign rental property.

How do I keep my records?

If you are required to register for MTD, you can maintain your records by using the following:

Accounting Software

-

These typically uses a bank feed to import transactions, which are then reconciled according to income or expense type

-

The quarterly submissions can be made directly from the software

- The software usually comes at a monthly subscription cost but include many features that could make running a business more efficient

Spreadsheets

- Your records can be kept on spreadsheets

- The quarterly submissions can be made using a bridging software, preserving the digital link

Will there be any penalties for late submissions?

For MTD, HMRC have announced that they will be using a points-based system for determining whether late submission penalties will be charged.

One point will accrue for each late quarterly submission, and a £200 penalty will be charged once an individual reaches 4 penalty points.

Any points accrued will expire after 24 months where the total number of points remain below the threshold. If the penalty threshold is met, points will expire after 12 months.

A £200 penalty will be charged for each following missed obligation after reaching the points threshold.

What we can do to assist you?

Firstly, we can sign you up for MTD online with HMRC.

If required, we would be happy to assist you with getting your record-keeping in place depending on which route you would prefer to follow:

-

If you will be using accounting software, our Bookkeeping Team can assist with the set up

-

If you will be using spreadsheets, we can provide templates to assist with your record-keeping

- If you will be using paper records, we can offer bookkeeping assistance

Once everything is in place, from July 2026 we can submit the quarterly submissions on your behalf, whether this be via accounting software or through our bridging software.

Finally, we can submit the end of year adjustments and tax return after the end of the tax year.

Making Tax Digital for Income Tax - webinar

Discover what the upcoming Making Tax Digital changes mean for you in this webinar presented by David Tallon and Sarah Wilson from our Private Client team:

If you have any questions about the above, or would like more information specific to your circumstances, please enter your email address below and we will get in touch:

Related View All

Our Accreditations and Memberships